Dear Republicans: There's Still Time to Make Health Care Great Again

Part 2: The Prescription

(My last article explained the problem Republicans face in trying to fix health care. This post focuses on the solution.)

We can’t afford not to have insurance because the prices are so high. But we also can’t afford insurance because the premiums are so high.

Which is why almost every American requires a significant subsidy from someone else in order to afford insurance – whether it’s government ACA subsidies, employer subsidies, or government-run Medicare, Medicaid and other programs.

With the COVID-era expanded subsidies for people on the ACA exchanges about to expire in a few days, there’s a growing panic among policy-makers about what to do.

You may have noticed that I’ve been warning Republicans in recent articles about the pitfalls of the various proposals reportedly under consideration. Their response back is understandable:

So what's the plan?

This article is my answer to that question.

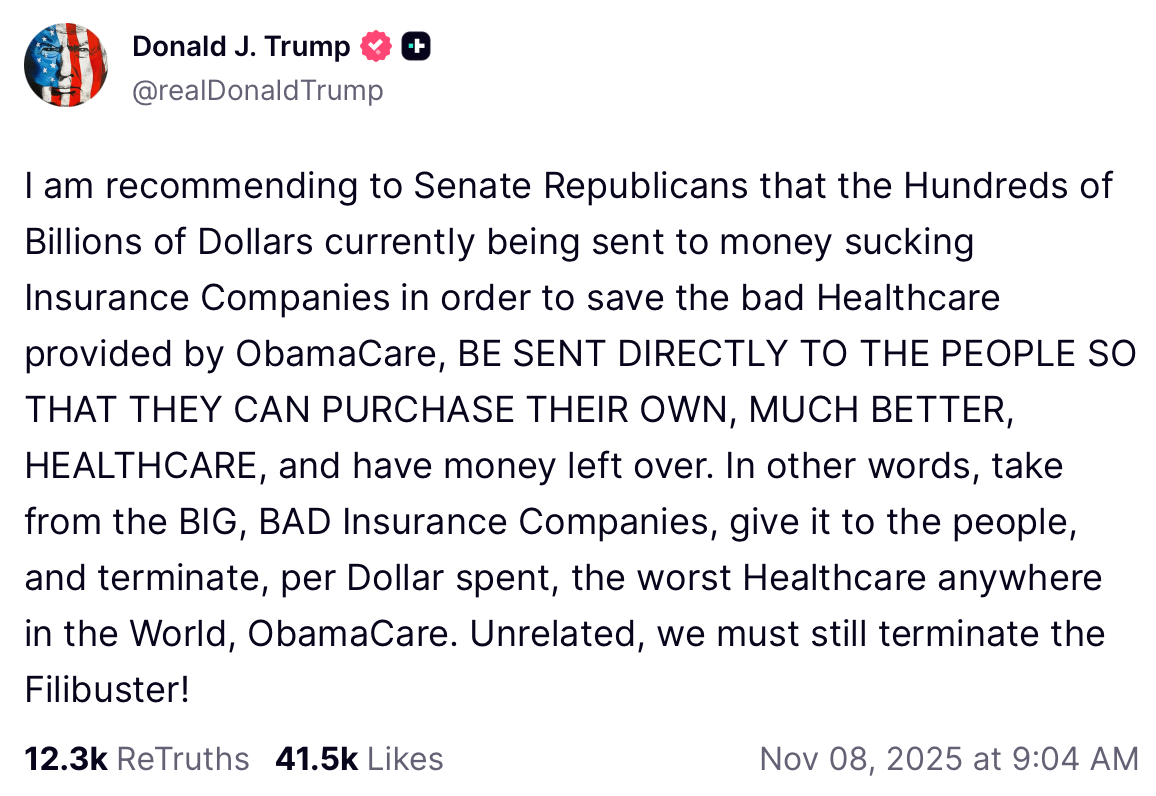

My proposal is the same as the president’s.

(But not the weak-sauce version being kicked around by some in Congress.)

So what details would put flesh on the bones of the president’s all-caps social media screeds against insurers?

Is there hope for a bill that can pass – satisfying both the moderates and the conservatives in the party, without screwing over voters and losing elections?

Answer: YES.

One of the problems with most Republican proposals is that they are only targeting the small fraction of Americans on the ACA exchanges. That’s 23 million people – a lot, to be sure. But 180 million Americans – almost 54 percent – get their insurance on the job, nine times more than ACA enrollees.

You can do a lot in the ACA market, but it’ll never move the broader health care needle – it won’t drive down prices charged by most hospitals and doctors, which are driving premium spikes.

That said, we still have to have a solution for the affordability problem for those 23 million currently on ACA plans. Because the premiums are so astronomical, almost all (92%) of those people are receiving free or heavily subsidized coverage, paid for by you and me.

That government cash goes straight from the Treasury to the deep pockets of the “money-sucking insurance companies,” to quote President Trump (he’s not wrong!).

As I’ve mentioned in previous articles, if we take money away from people who are currently getting subsidies, we will lose the mid-terms, period. We lost the 2018 mid-terms just for trying.

No amount of wailing and gnashing of teeth from conservatives will change this. I wish it weren’t true, because it’s extortion. But it is true.

If we lose the mid-terms, Democrats will come in and make things even more impossible the next time we’re up at bat for a chance to fix this.

So here’s my four-point plan, or rather, what I think the president might have meant with his social media posts.

Let’s start with the executive summary, followed by a deeper dive for the bravest among you.

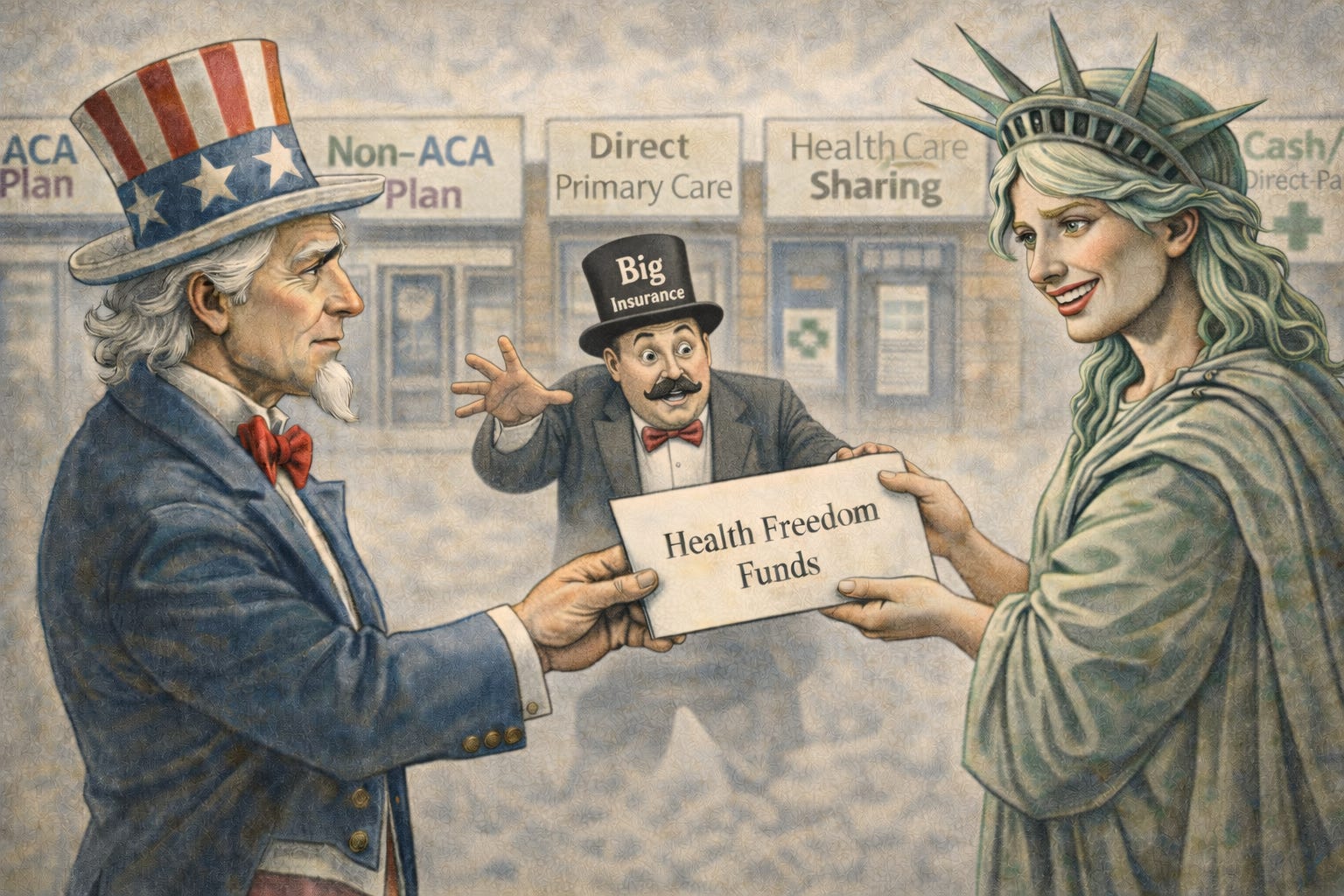

School choice for health care: ACA Market edition

Convert all subsidies currently going to insurers on behalf of ACA exchange enrollees into dollars put in a tax-advantaged Health Freedom Account, or “Health Wallet,” “Care Fund,” “MediStack,” “Trump Card,” whatever branding you choose. It’s an account owned by the enrollee. For now we’ll call it an HFA.

They can use the money to buy the same plan they’re on now, a different plan, a plan off the exchange, a membership like a health care sharing ministry or direct primary care, or just cash-paid care.

Trust them to choose their own health expenses, including holistic care, without the government dictating what medical care is or should be.

Let anyone else contribute to it as well, up to the max subsidy amount available for an ACA silver plan, or whatever cap above that Congress decides on (see below).

School choice for health care: for everyone else

Allow everyone in America to have an HFA - including employees of businesses. That way, employers who want to provide financial support for their people – but don’t want to be in the health care business, having to manage a complex group health plan for their workers – still can provide robust health benefits. By contributing to their workers’ HFA, businesses could free up employees to make their own health choices rather than having their bosses make those choices for them.

Cut out the middlemen between buyers and sellers of care

Require doctors and hospitals to publicly post and accept a cash price for all services that is equal to or lower than the lowest carrier rate.

End discrimination against uninsured patients by requiring providers to treat cash-paying patients the same way they would patients using insurance.

Prohibit insurance contracts from banning employers or doctors from cutting out the insurer and negotiating a better deal directly between themselves, or simply transacting in cash on behalf of patients.

Prohibit state/local laws from banning new hospitals and repeal federal law prescribing who can own hospitals, like doctors.

Require pharmacy benefit managers and third party plan administrators to assume fiduciary obligations to the plans and enrollees they serve.

End secret health care prices

Codify the first-term Trump price transparency rules and supercharge them with more details, more ease of access, and excruciating penalties for noncompliance.

Entitle all buyers of health care to have full access to their claims data, including individual patients, employers, unions, and governments, again, with excruciating penalties for non-compliance.

That’s it, that’s the plan.

You’ll note that I’m proposing to extend a form of the COVID subsidies.

Conservatives don’t want to do this. I know. I hear you. I don’t want to either.

But I like winning elections, and I know you do too. We have no margin in the House – every moderate in a swingy, unsafe seat has to vote for a package in order for it to pass.

Moderates are currently signing up for a totally clean (i.e. reform-free) three-year extension of the subsidies right now. That would get us all the current costs and no policy wins in return, enshrining the premium-spiking death spiral we’re in now.

Moderates have rightly figured out that they have to extend the subsidies or they’ll lose their seats. I don’t want them to lose. Do you want them to lose?

Conservatives in safe seats have to sacrifice our principles more than moderates do, when margins are this tight. I’m sorry. I wish it weren’t so.

However, if it’s any consolation, this is one of the only proposals that actually would lower costs throughout the entire commercial market (not just the ACA exchanges), because it would facilitate actual price competition and greater efficiencies through cash/direct-pay and direct contracts between employers and hospitals.

I urge you to consider that, if prices come down through these reforms, premiums would come down too, including the silver benchmark plan premium that subsidies are tied to. In this way, there’s a path for the extended subsidies in this proposal to actually pay for themselves in lower health costs nationwide.

Moderates, you get to say you took nothing away from anyone and you gave them more options, more control over their own destiny, and more affordability.

Conservatives, setting cost aside, you’d be getting all your health policy hopes and dreams.

Conservatives have long wanted to move subsidies into private accounts, to give people choices away from the limited government-approved options in Obamacare, and to move employers away from defined benefit health coverage towards defined contribution coverage. This proposal would do all of those things.

My experience is that you can actually get big policy reforms done in Washington. But you always have to buy them. Meaning, you have to spend more than you’re comfortable spending. That’s usually the compromise, and I’ve found that it’s generally worth it, if your policies are the right ones.

So that’s my pitch. And now here’s the deep dive.

If you want to look under the hood a bit more...

1. SCHOOL CHOICE FOR HEALTH CARE - ACA market edition

All current subsidies going to anyone on the ACA exchanges will continue flowing, but they will be given to the people themselves, not the insurers, so that the people can buy whatever health care or coverage that they want.

Put all subsidies that any American qualifies for today (including base ACA subsidies, COVID expansion subsidies and Cost-Sharing subsidies) into an HFA.

The amount that goes in is the exact amount of the max subsidy that the person would qualify for today under the ACA for an average silver plan. This amount changes every year based on the rate of inflation or some other standard index, rather than just a blank check covering whatever insurers feel like charging.

HFAs can be used, tax-free, for:

Insurance premiums for ACA exchange plans (people can buy the same plan they’re currently on if they want)

Insurance premiums for off-exchange insurance plans

Membership fees for Health Care Sharing Ministries

Membership fees for Direct Primary Care

Out-of-pocket insurance-related expenses such as deductibles, coinsurance, copays

All other qualified medical expenses under Sec 213(d) of the tax code, EXCEPT abortion or sex-rejecting (transgender) procedures.

No one loses a single dollar that they currently are getting in subsidies (i.e. it’s an extension of the COVID subsidies, only through a different mechanism).

If you are on an ACA Blue Cross plan today and Blue Cross is receiving your subsidies, you will now get those subsidies in your HFA. You can take that money and give it right back to Blue Cross to buy your same plan. You lose NOTHING.

But if you want a different plan, like say, an off-exchange plan or a health care sharing ministry membership, you can use your subsidy money to buy that instead, and keep whatever’s left over in your HFA for other medical expenses.

NOTE: If Republicans insist on ending the expanded (COVID-era) subsidies, I recommend that they only do so for the richest people. Pick a threshold that everyday Americans would all agree is “rich” (and therefore, fair), say, above $150,000 or $175,000.

ANOTHER NOTE: Ok, ok, what about phasing down the COVID-era subsidies after a few years? You could maybe get them down to pre-COVID era – or even lower over time. Unlike most reform plans, this one actually rescues the rest of the commercial market and not just the ACA – that means that underlying prices will now be subject to competition at scale. That could lower premiums and save money in the end by lowering the indexed subsidy amount allowed in the HFAs each year.

AND YET ANOTHER NOTE: It’s important – both politically and morally – to prohibit HFAs from being used to pay for stuff that is violent toward self and others like abortion and sex-rejecting procedures like cutting the breasts off little girls. That’s not health care – conventional, holistic, woo-woo or otherwise. Sorry, not sorry.

Goodies for MAHA

Little-known fact – you could use the HFA for MAHA tax breaks.

HFAs could be used, not just for insurance premiums or membership fees, but for “qualified medical expenses,” as defined by the tax code. That means it could also include expenses that help you live like a human, like physical training, visits with an acupuncturist, Traditional Chinese Medicine practitioner, a functional nutrition expert, a fertility health coach, and so forth.

BUT here’s the proviso – to comply with current IRS rules, you would need to get a licensed clinician to write a letter of medical necessity saying that the clinician is prescribing these less-conventional services or equipment in order to treat a specific diagnosed condition like obesity, depression, lower back pain, infertility, and so forth.

In other words, tax breaks for MAHA.

This policy would make things a lot more fair for people like me, who are more woo-woo, and don’t want insurance at all.

More and more Americans are extracting ourselves from the white-coat religious cult and would prefer to treat with time-tested home remedies, and pay cash if we need to set a bone or get an x-ray.

But since catastrophic care is still so unaffordable, maybe we join a health care sharing ministry in case we’re attacked by radicals on a college campus and need a burn unit or ICU.

If Congress really loved freedom and respected the medical choices of Americans, these HFAs wouldn’t be restricted to only government-approved practitioners and therapies.

Further, why not let us donate unused money in our own HFA to someone else’s health care whose costs exceed their HFA limit?

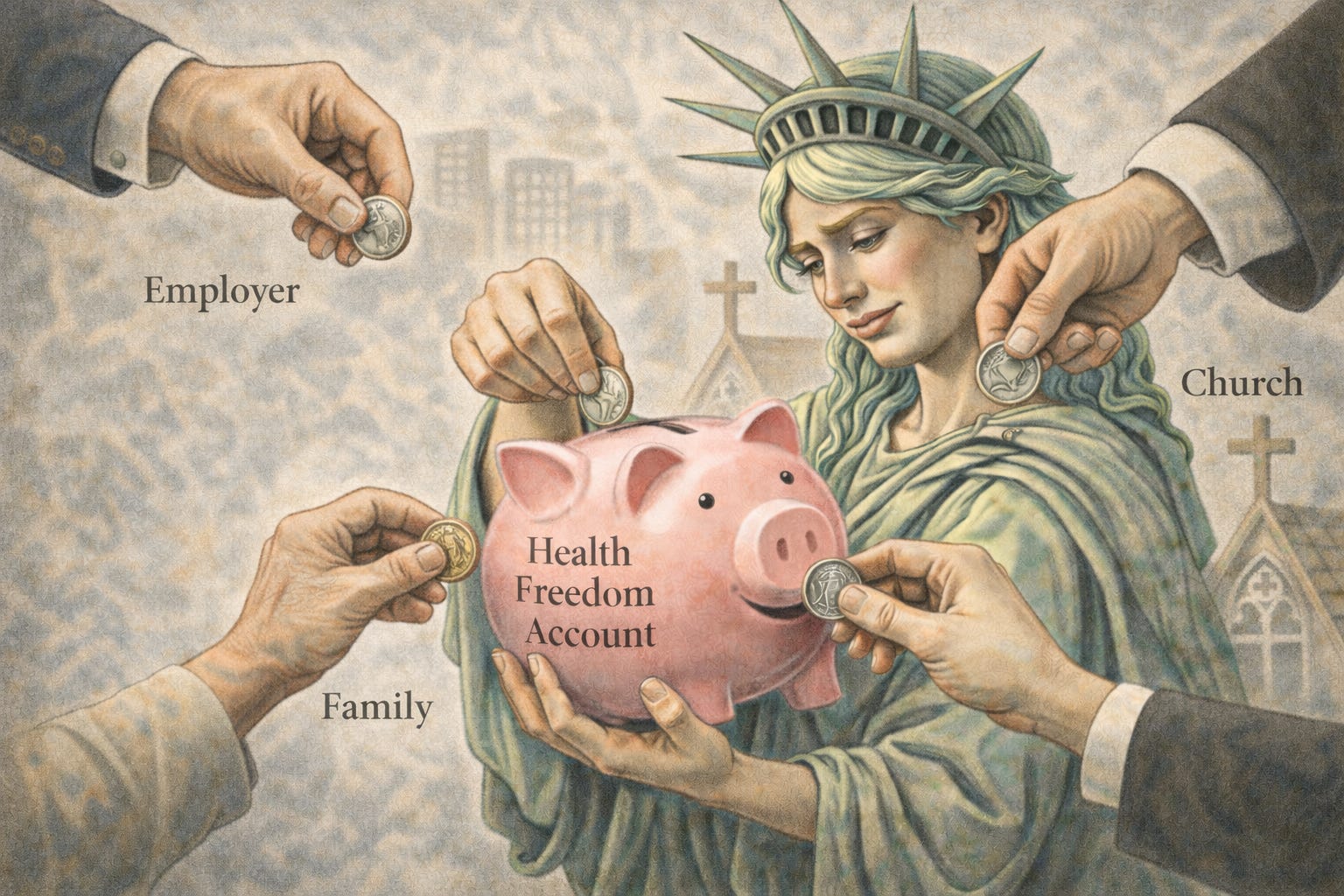

2. SCHOOL CHOICE FOR HEALTH CARE – for Everyone Else

Why not open up HFAs to all Americans, not just those currently getting ACA subsidies?

Remember those 180 million Americans getting their insurance on the job? This has turned every company into a health care business – whether they want to be or not. What if they could get out of that business and focus on their core competency, while still helping their workers afford health expenses?

HFAs would not only be available to people getting subsidies today. HFAs would be available to anyone else (only without the government pre-funding).

This would build on a policy created by President Trump in the first term where employers were allowed to set aside money for workers to buy their own coverage rather than buying it for them.

Anyone could contribute private money to the HFA – tax free to them and tax free to the account-holder – up to a cap equivalent to the amount most people would use for an insurance premium and out-of-pocket costs. Another cap could be used instead, such as the maximum ACA subsidy amount.

That private money can be contributed by the account owners themselves, or anyone else on behalf of the account owner, including employers, health care sharing ministries and other charities, crowd-funding sites, churches, or family members.

Employer-sponsored health benefits are already tax free, so putting that same money into a worker’s HFA won’t drain the Treasury - well, not anymore than it’s already drained.

3. CUT OUT THE MIDDLEMEN BETWEEN DOCTORS AND PATIENTS

There’s a hostage crisis in the 180 million-person employer market. Secret contracts with middlemen keep prices high for ALL Americans by prohibiting buyers and sellers from making better deals with each other - directly.

America’s health care system is full of good doctors, nurses, and (a few) hospitals. American businesses want to do the right thing by their employees, but they’re drowning in double-digit rate hikes year over year, threatening their ability to survive in the economy and compete with foreign companies.

Charities, churches and health care ministries just want to help patients get care at affordable rates.

But one group quietly controls the entire system: health insurance companies.

Insurance contracts hold every stakeholder hostage.

Behind the scenes, insurers use their contracts to lock up doctors, hospitals, employers, ministries and patients – all to block competition.

And if you’re wondering exactly how they carry out their dirty work, these contracts:

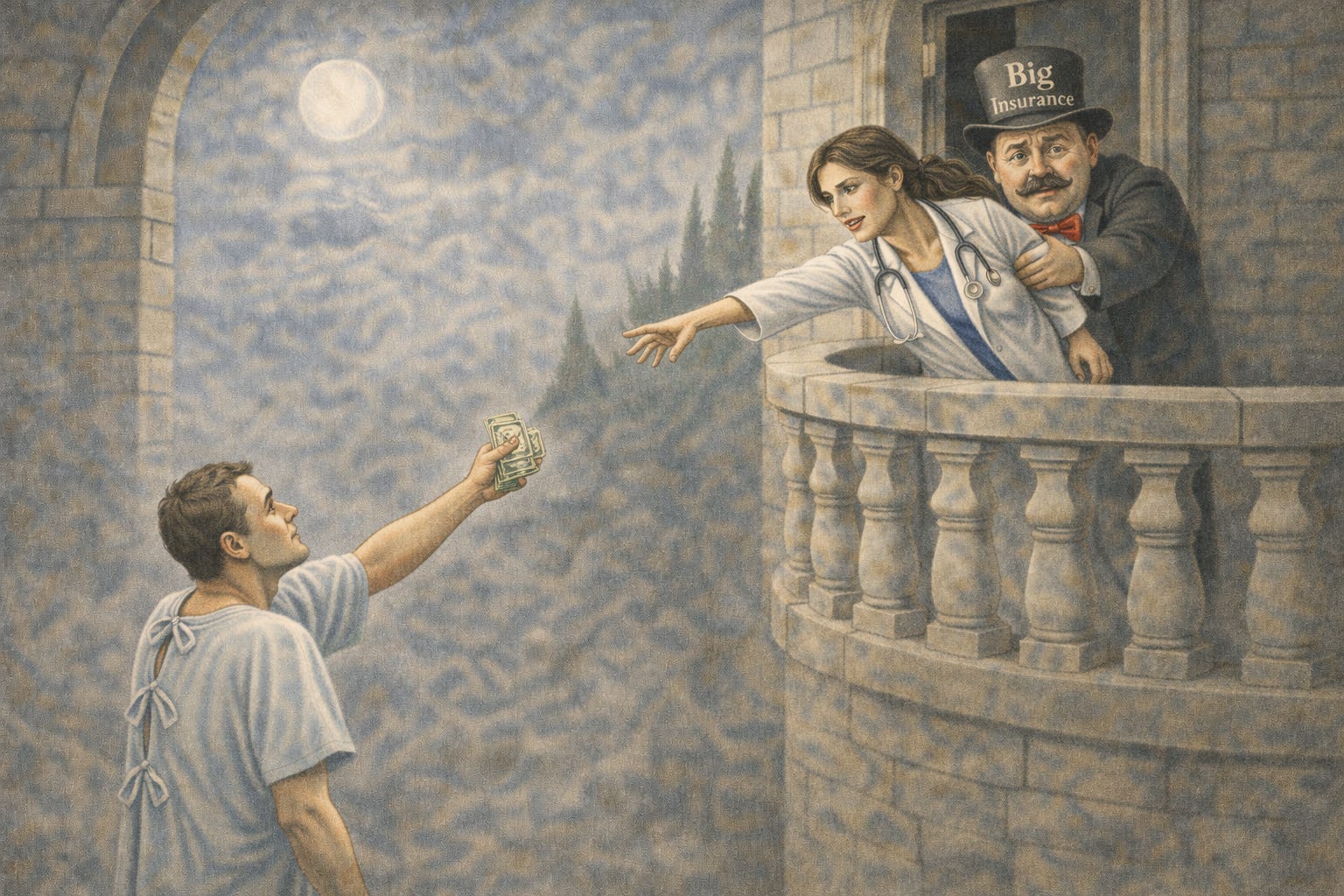

✘ Stop hospitals and doctors from accepting fair, lower direct-pay prices from patients:

Even when a doctor wants to accept a lower direct price for someone paying cash, the insurer contract often forbids it.

When patients who are enrolled in one of my employer-client’s plans show up at a doctor’s office, they are asked to present their ID card. If that ID card has a carrier logo on it, then that doctor isn’t allowed to accept cash from us for a lower price. He has to send the bill to the insurance company and charge us those predatory rates. And we’re not supposed to even offer cash in that situation either, because of our own contract with the carrier.

We’re all held hostage to this middleman.

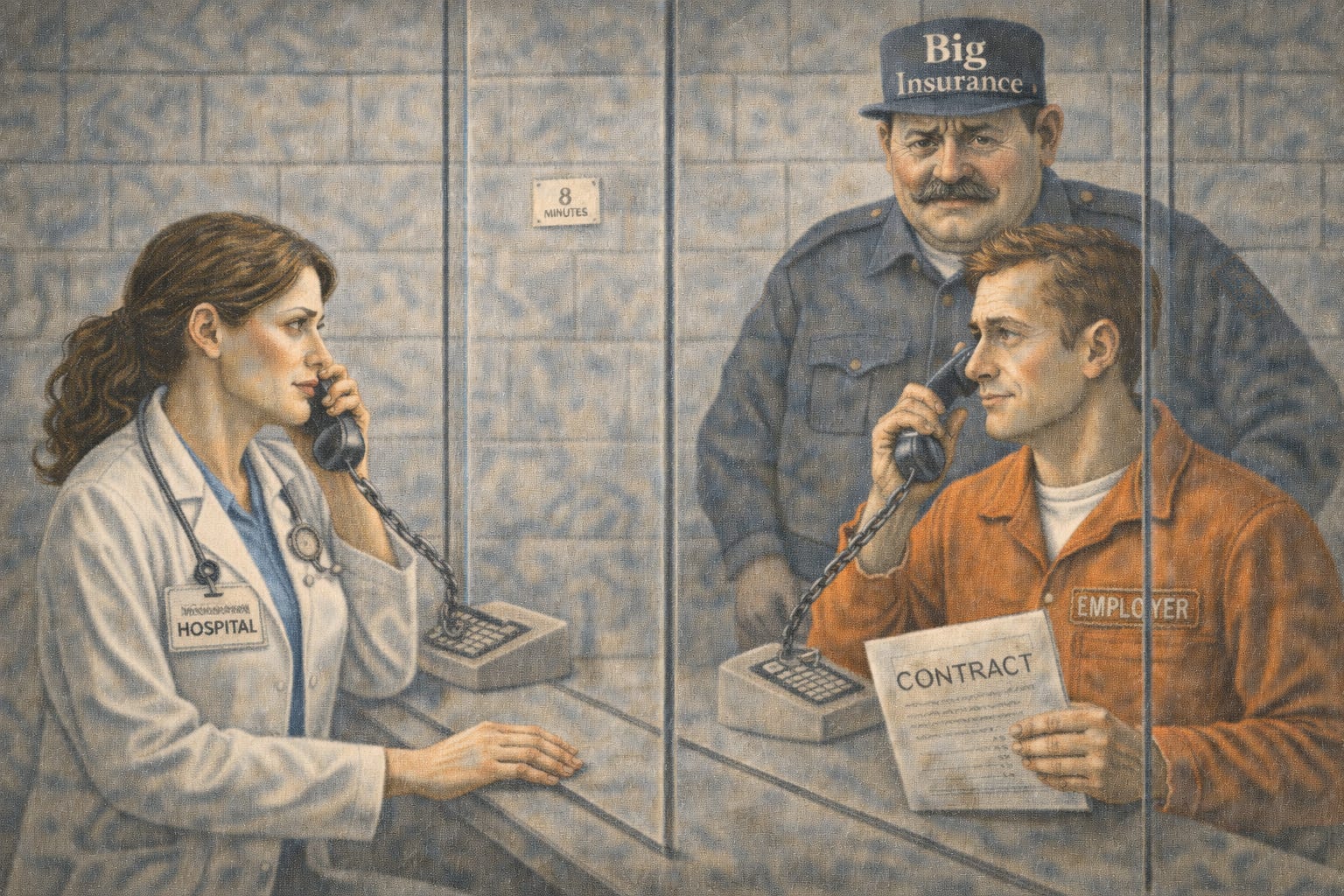

✘ Stop doctors and hospitals from giving employers a better deal without the insurance network.

If a local employer wants to contract directly with a hospital for lower prices, insurers often ban the hospital from saying yes. Employers are hostage to the insurer’s deal—even when everyone knows the insurer negotiated a terrible one.

My employer-clients often want to do a deal with their local hospital. But both my client and the hospital have their own separate contracts with, say, Cigna. We have to get permission from Cigna to do that deal. If the deal is too likely to disrupt Cigna’s profiteering, they veto the arrangement and we’re both out of luck.

✘ Stop patients from getting appointments unless they have the “right” insurance.

One of my employer-clients isn’t an employer at all, they’re a religious order of Catholic nuns.

They wanted a health plan without a carrier network so that they were free to pay cash directly to doctors or hospitals, or to negotiate their own contract.

Just last month, NYU hospital (a so-called “charity” that doesn’t pay taxes) told a desperately sick nun, “sorry, we won’t let you in the door because your ID card doesn’t have a carrier logo on it. Even though your plan will pay. Even if one of our doctors very much wants to see you.” I had to use my fancy DC connections to get hold of an NYU executive, just to be allowed to pay cash at the door, before this poor sister could be seen. By the way, this sister would qualify for Medicaid and NYU’s financial assistance program. We actually wanted to PAY the hospital instead of going that route.

If you want to pay out of pocket — or if your employer or health care sharing ministry wants to pay on your behalf — you should be able to get the appointment.

✘ Punish doctors if they offer lower prices to anyone else. Insurers often include:

“Most-favored-nation” (MFN) clauses – requiring the doctor or hospital to give the carrier the best price compared to any other purchaser, no matter what.

“All-products” clauses – requiring doctors to participate in every network offered by the carrier if they want to participate in one.

“Anti-steering” clauses – prohibiting employers from steering patients to doctors outside the network who are higher quality or lower cost.

Outright bans on doctors or hospitals offering lower prices outside an insurance network.

These contract provisions block doctors and hospitals from giving anyone a better deal — patients, employers, even charities like my nuns.

This is anti-competitive behavior and should already be illegal under antitrust laws.

Congress should make it explicitly illegal once and for all.

To put an end to these gangster tactics by insurers, Congress should:

✅ Require a direct-pay option for all care

Every health care provider must post and accept ONE single “direct-pay price” for each service – the same price for every patient, employer, or non-insurance payer willing to direct-pay, upfront and in full.

The published direct-pay price must be equal to or lower than the lowest commercial insurance rate accepted by the provider. Insurers lose the power to keep cash-paying customers or employers from getting a better deal. Being paid cash upfront and in full eliminates the need for pre-certification, eligibility checks, chasing patients for their cost-sharing obligations, sending claims, waiting around for payment while the insurer makes billions on the interest earned by delayed reimbursements, and collections efforts. That’s why it makes sense that the direct-pay price without all that bureaucracy and inefficiency should be equal to or lower than an insurance rate.

NOTE: Providers should still be allowed to negotiate a hardship discount between doctors and patients.

✅ End discrimination against cash-pay patients

Congress should ban the practice of turning away direct-pay patients, or otherwise discriminating against them, such as refusing to schedule, delaying an appointment, putting you at the back of the line, requiring you to use insurance if you have it, requiring you to submit claims to your insurance first, imposing any extra hoops or extra steps, simply because you (or someone paying on your behalf like your employer or a ministry) are willing to pay the posted direct-pay price.

✅ Establish a right to cut out the middleman between the buyers and sellers of care

Insurance contracts with health care providers (or employers) can no longer prohibit:

Direct contracts with employers

Direct contracts with health care sharing ministries

Community-based arrangements between a local hospital that’s part of a giant conglomerate system and its surrounding community of employers or patients

Lower-rate contracts outside insurance carriers

New payment innovations that insurers historically block or control, such as subscription-based models or bonuses for achieving certain clinical outcomes.

Hospitals and doctors can finally say, “yes, we’ll give your business or your ministry a better deal than your insurer does.” Insurers lose their veto pen.

✅ Ban state “certificate of need” (CON) laws

CON laws are truly cons. They give state and local governments, as well as competitor incumbent hospitals, the power to ban new hospitals from being established in communities. These CON laws are anticompetitive clap-trap designed to protect predatory price-gougers from competition.

✅ Repeal the ACA’s ban on physician-owned hospitals

The Democrats who wrote the ACA thought that fat-cat MBA executives are somehow less self-interested than doctors would be when it comes to hospital revenue. This is crazy. Those of us trying to contract with doctors and hospitals on behalf of employers know that the very best facilities are the ones that are owned and run by the physicians who practice in them. They also happen to be the most willing to contract with employers, health care sharing ministries and cash-paying patients. I wonder why incumbent hospitals might not want that in their communities?

✅ Make PBMs and TPAs fiduciaries again

Middlemen often buy each other up to become bigger, grosser middlemen. This has happened with insurance companies buying up pharmacy benefit managers (PBMs) and vice versa. So then you have the situation where the profiteering gets even more opaque and harder for employers and other plan sponsors to see or avoid.

Insurance companies serving as third-party plan administrators (TPAs) might pretend to have low or transparent fees with their employer-clients. But they’re profiteering on the PBM side of the house and not telling you. They are driving up your costs and screwing you in more ways than a poor HR manager or even the best benefits advisor can suss out.

Worse, when employers do figure this out and then sue, too often they get told in court that these entities didn’t have to act as prudent fiduciaries — that was all on you, so too bad, keep paying them money to rape and pillage your workforce. These court cases have often been preempted in the first place by contract provisions forcing disputes into arbitration rather than the cold light of the court record.

It’s time to give guidance to courts who have been all over the place on this. Congress should set the record straight: make it clear that, when PBMs and TPAs exercise discretion that could help or harm plan beneficiaries, or when they act in their own interest rather than the plan’s, they’re fiduciaries and they can be sued like one. This will force the lawyers at these giant corporations to clean up their act and could bring sanity to the transactions and contracts that are bankrupting all Americans.

4. END SECRET HEALTH CARE PRICES

President Trump’s health care price transparency initiative, which we described in a previous article, required secret prices to be publicly available for the first time ever. Congress should enshrine those rules into law so that it’s harder for the industry special interests to undo them (they’re always trying!).

They should be beefed up even more, and enforcement penalties for noncompliance should be excruciating. Right now, penalties are basically a slap on a wrist or nominal fines.

What’s more, any purchaser of care – a patient, an employer, a union, or government program – should be provided the absolute right under the law to demand and receive all their claims data, every single raw data field, including the sticker price, the contracted rate (or the out-of-network allowable amount), the paid amount (including all extra fee shenanigans on top of contracted rates), rebates attributable to a given drug, and every single other data point associated with that claim.

This is essential so that the people that, you know, buy the stuff know what they’re paying so they can make sure they’re getting the best deal (SPOILER ALERT: they’re not!). Getting the best deal is actually required under the law for fiduciaries like employers but these middlemen are preventing them from complying.

More excruciating penalties should be imposed on any middleman holding claims data who does not turn it over within 24 business hours of the request.

I have had to get lawyers involved to get claims data out of these douche-bags for my employer-clients — and this protracted fight has taken — by design — months and months before the middlemen give in, and then they usually turn over garbage data, and well after it’s too late for the client to make the decision to fire them that year.

This chicanery should be illegal, immediately.

The Fifth Step of the Four-Step Plan

If you’ve made it this far, first of all, thank you for being a paid subscriber. Second, you obviously care deeply and so I’m going to ask you to, well… pray.

Health care is so personal, so intimate, so scary, so important. We have to get it right, and it’s so hard.

It’s a multi-trillion dollar industry, a fifth of the economy, and controlled by almost demonic forces profiteering off the suffering of the American people.

The expertise that’s necessary to understand it all is held by no one, nowhere, least of all in Washington.

So it’ll take divine intervention to redeem this industry and make health care great again.

Let’s bow our heads together.