Outsmart the Medical Billing Trap

A step-by-step patient playbook for paying what's fair — and not a dollar more.

A quick note before we get into it.

My last couple of articles were in the weeds — PBM reform, insurance market mechanics, the government shutdown drama — the stuff that makes benefits advisors and policy wonks nod along.

This one is for everyone else.

And for the experts on the inside, this is the article you send to your mom. Your neighbor. Your buddy who just got a $14,000 bill for an ER visit where they gave him Tylenol and told him to follow up with his doctor.

This is for the people you love who are still getting taken advantage of by these corporate conglomerates — the people you won’t always be around to fight for.

I have a dream… that one day there will be a single, transparent, competitive cash price for every health care service, with no games, no exploitation and no financial abuse. Until then, consider this a cheat sheet. Print it out. Send it to everyone you know. Stick it on the fridge. Because the system is not going to hand patients this information voluntarily and they freaking need it.

For those of you who don’t know me yet… Hi! I’m Katy.

I’ve spent enough years inside health care policy to figure out exactly where and how the money moves.

I've been in this fight from the Senate, the White House, my sister's hospital bed, my granddaughter’s birth, my own home office. I've worked on Medicare reimbursement rules, negotiated with hospitals, fired insurers, and helped write the laws that were supposed to protect patients from price gouging and surprise bills.

I understand how claims get paid, how hospitals set prices, and how the contracts between insurers and providers actually work behind the scenes.

And even with all of that knowledge, I still get gouged if I don’t walk into the system loaded for bear.

No one is immune.

Because the system is built to assume your inattention — and to exploit it. So if you show up passively, sign whatever they put in front of you, and assume the bill that shows up six months later is what you actually owe, you will almost certainly overpay.

Not by a little. By a lot. It’s practically guaranteed.

Here’s how they run their scheme:

You’re in the ER. You’re in that gown — the paper napkin designed to make every human being on earth feel like a large, drafty toddler. You’re in pain, or scared, probably both. A girl about 20 years old wheels her computer over to your bedside: “I just need you to sign a few things while you wait for the doctor.”

Then you sign. Of course you sign.

Because you’re sitting in an emergency room and this is not the moment you expected to become a contract attorney. So you just do what you’re told. You submit. That’s exactly what they’re counting on.

If you’re not in an ER, but rather a doctor’s office, the assault might come in the forms given to you on an iPad rather than the workstation on wheels.

Buried in those forms is your consent - not just to be treated today, but to be charged whatever they feel like charging. To assent that, whatever your insurance doesn’t pay is on you. At whatever price. Regardless of what’s fair (or if you can afford to pay it). Because the billing Borg spits out whatever price it wants (or thinks it can get away with), and you just signed away your right to argue about it later.

I know this because I helped write the very rules that were supposed to stop this practice. Most of you have no idea those rules exist — much less that they handed you actual weapons.

So let’s fix that — right here, right now. What follows is your step-by-step guide to stopping the pillage.

Before You Walk In: Know More than They Do

When you go to the manicure place, they have a price list on the wall. The grocery store. The salon. The dry cleaner. All have prices visible before you buy. But health care? That’s a complete secret.

We couldn’t possibly tell you what this costs. It’s too complicated. And we know you’ll be too scared to walk away, so pay us a little deposit, sign these forms, and don’t you worry your pretty little head about what comes next - we’ll make sure you know how much you owe… later.

Yeah, no.

Here’s what you do before you set foot in that facility (unless it’s an emergency of course, but don’t worry we’ll cover that too).

Get the billing codes

These codes are what you’ll use to figure out what’s considered a reasonable price for the specific thing you are having done. Sounds complicated, but it’s not as hard as you might think.

Call the doctor’s office (or hospital or other facility) you plan to see and ask: “What CPT codes are you going to bill for this?”

CPT codes (pronounced C-P-T) are the billing codes attached to every single thing they do to you since your electronic medical record is basically a glorified cash register. (That’s also why the doctor’s always staring at a screen instead of looking at you. Every click is a charge.)

And when you ask, the front desk may not immediately know what you’re talking about. Don’t let this bug you. They’re not dumb people — they’re just not trained on this, because the system prefers you don’t ask. Be patient. Persist. Someone should be able to provide them. Your new favorite phrase: “I’ll wait while you find out.”

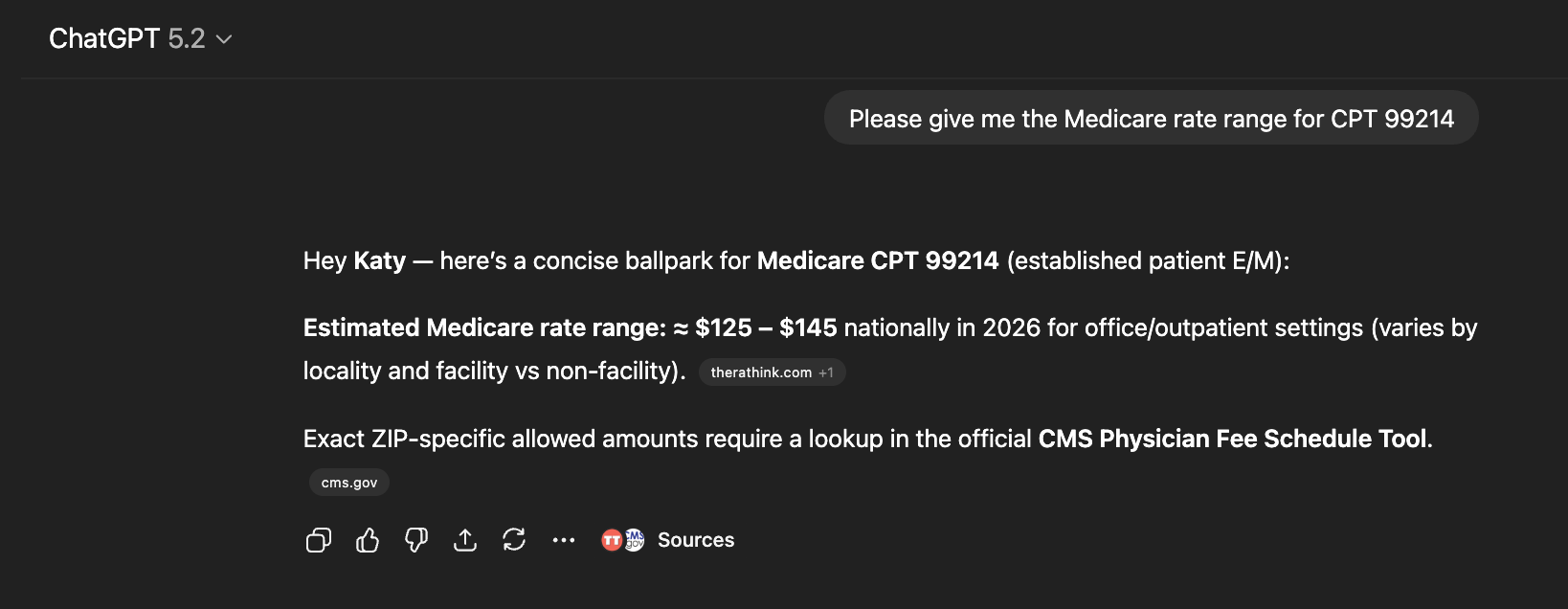

See how much Medicare would pay for each code

This is how we start to figure out what’s considered reasonable.

When you get the codes, throw them into the Medicare Procedure Price Lookup tool, or even easier, into ChatGPT, and ask for a Medicare rate range. This gives you the baseline cost.

And while you won’t usually get away with paying the Medicare rate as a commercially insured patient, you will use this to smell a gouge from across the parking lot.

Crunch the numbers.

Here’s the math that allows you to decide what’s reasonable.

Most people think health care pricing is complicated. It’s not, really. It’s just opaque. The Medicare rate is the closest thing to what a procedure actually costs, and many in the industry base their prices as a multiple of it.

A good price is 125–150% of the Medicare rate. A 25–50% markup above cost. You should always start here.

A fair price is 150–200%. This is what smart employers often aim for.

A predatory price is anything above 250%.

Keep this framework in mind anytime you evaluate pricing. The framework varies based on type of service, but this crude scheme will generally serve you well.

The average commercial price for outpatient services? 250% of Medicare. And an inpatient hospital stay? 300%. That’s the average. So if you’re wondering whether you’re getting gouged — you are. You just didn’t know it because nobody ever showed you the math.

Side Note: If you want to go full nerd (and I know some of you do) Patient Rights Advocate has a free tool that lets you download your hospital’s price transparency files — the ones they’re required to post publicly. You’ll get a spreadsheet. Search it by CPT code, find the column for your insurance plan, and now you know what they told the government they’d charge your plan. Other free tools worth bookmarking: Sage Transparency and Simple Healthcare. Which is all useful ammunition for later when the bills show up and the numbers don’t match.

Now you know what’s “reasonable.” But we’re not quite done.

Ask about “site of care.”

You can get the exact same surgery, often with the exact same doctor, at a wildly different price — depending on where they physically do it. Meaning the same surgery, by the same doctors, with the same anesthesia costs different amounts depending on where it’s performed.

Any place owned by a hospital charges a facility fee on top of everything. And “owned by a hospital” doesn’t mean it looks like a hospital. It might look like an office building, a strip mall or a converted Pizza Hut (not making this up). If you see a hospital logo on the intake forms, the building, or the website — you’re paying the hospital tax with an extra facility fee. You have to ask.

So ask your doctor: “Do you also do this procedure at a freestanding facility?”

Freestanding imaging centers, freestanding labs, freestanding surgery centers exist everywhere. Asking is how you find them.

One of the AllBetter subscribers learned this the hard way and then pivoted in self-defense. She needed an MRI, but her insurance said she couldn’t schedule one within thirty days of an upcoming, unrelated colonoscopy. Rather than get tangled in the authorization nightmare — which would’ve pushed her into the new year and a new deductible — she called around, found a freestanding center, and paid cash. Her cash price for an MRI and two X-rays was less than she would have paid using her insurance plan. Same day. No authorization. No drama. This is NOT uncommon.

Find out how many people are going to bill you.

Most people think their surgeon is the only one who’s charging.

But there’s probably an anesthesiologist. A pathologist reading the biopsy. A radiologist — possibly in a different time zone — sending a separate bill. Even in the ER, the hospital and the ER doctor who saw you for exactly 2.5 minutes bill you separately.

Ask upfront so you’re not blindsided later: “which facilities and professionals will be billing me for this procedure?”

Get a Good Faith Estimate.

Under the Consolidated Appropriations Act of 2021, they’re required to give you a Good Faith Estimate of all the charges for your service no later than three days before the visit. They’re not legally bound to hit that number exactly, but they can’t wildly deviate without risking “bad faith," which isn’t allowed. The estimate gives you ammo in case they dramatically blow past it later.

Compare the cash price.

Especially if you have a high deductible you haven’t met.

Always ask: “What is your self-pay rate?” or “What’s your cash price?”

Some places will just hand you their sticker price (anywhere between six and thirty times the Medicare rate) and call it their cash price (which will look inflated because you’ve done the work comparing to percentage of Medicare). And when you spot it, just know that’s probably not their real cash price. It’s just them trying to dissuade you.

Then say something like: “That’s 350 percent of Medicare. You mean there’s no discount for me paying upfront, right now, day of service? No discount for not making you bill my insurance and wait six months to get paid something crappy?”

That usually recalibrates things.

And follow up with HR.

One reason that people don’t pay cash even though it’s way cheaper than their insurance rate is because they worry that this spending outside their plan will increase costs later in the year because it’s not applied to their deductible. After all — your plan can’t apply payments to your deductible that they didn’t know about.

This is a reasonable concern, which is why Texas and Tennessee have required plans to apply cash payments against deductibles. But even if you don’t live there, most employers can see the value if you bring it to their attention. Go to your HR department and tell them that the cash price is lower than the egregious rate their stupid carrier charges them and ask them to apply your cash payment to your deductible. They may claim that they can’t do it, but if they’re a larger “self-funded” employer (which is almost all employers over a few hundred employees), they’re wrong. Tell them to make the request of the plan on your behalf — remind them that the value prop that their carrier is selling is to get better rates for health care than they could get without the carrier.

One more thing on cash pricing — doctors are contracted with your plan if they’re in network. That contract usually prohibits them from accepting cash for a patient that they know is covered by the network plan (which is why I propose to outlaw those contract provisions in the plan described in a previous article). So ask them about their cash price before you’ve shown them your ID card. If you’re already their patient in their system, tell them your insurance has changed and you’re now a self-pay patient. You can always change back later when you don’t want to pay cash in the future. That helps them check the contract box.

A few special cases to consider:

Watch the calendar. Your deductible resets January 1st (probably - some plans do this mid-year, so you might check if you’re not sure). Pre-op labs in December and surgery in January = two deductibles. If you have any control over timing, keep everything in the same calendar year.

Check for financial assistance. Almost every hospital is required under the ACA to have a financial assistance program. They’re also required to tell you about it. Most don’t. And some have been caught actively hiding it and bullying employees not to mention it to needy patients.

Google: “[hospital name] financial assistance program.”

If your household income is under roughly 400 percent of the federal poverty level — around $132K for a family of four — you may qualify even if you have insurance. And if you do, under the program, they must charge your out-of-pocket costs based on “amounts generally billed,” a formula weighted toward low-paying programs like Medicare, Medicaid and the VA. Translation: your $800 out-of-pocket obligation might drop to $300.

Once you have a bill, be sure to ask the hospital about financial assistance. If you’d like help with this, one of the greatest charities in the world is DollarFor.org — they erase medical bills by helping you apply for the charity program and getting that bill reduced or eliminated based on your income. For the same procedure. Same hospital. Same doctors. Just different math - because you asked.

The Day Of Service: How to Evade Their Trap

You’ve done most of the hard work at this point, by figuring out what price you should expect to pay, whether’s it’s reasonable, whether cash or charity might be a better solution. (I promise, it’s downhill from here.)

Now it’s just you, that drafty gown and that darn iPad the nice lady just shoved in your face. And the best way to deal with that pesky screen is to get rid of it altogether.

Ask for paper forms.

You are allowed to. They won’t love it. They’ll be discombobulated or annoyed. That’s a them-problem, not a you-problem.

“I’d like paper forms please. I don’t mind waiting.”

If they push back, act confused, or start giving you a hard time, escalate: “You are required to give me paper if I ask for paper. I’ll wait.”

Because you can edit paper. There are two forms you need to pay attention to:

The “consent to treat” form isn’t just consent to treat — it’s your consent to be gouged at whatever rate they choose, with you on the hook for whatever insurance doesn’t cover. No ceiling. No recourse. No bueno.

The No Surprises Act disclosure is supposed to explain your right not to be surprise-billed by out-of-network professionals you didn’t choose — the anesthesiologist who wandered in or the radiologist reading your scan from New Zealand. But instead, the form often asks you to waive those rights (yeah, we’re not doing that either).

How you handle them depends on where you are.

If you’re in the ER, they must treat you no matter what you write on a piece of paper. So edit freely. Every time you see the word “amounts,” cross it out and write: “reasonable amounts not to exceed 150 percent of the Medicare rate.” Then sign it. On the No Surprises form, sign nothing. It is supposed to be a notice of your right not to be screwed. If they’re asking you to sign something, it’s to get permission to screw you.

If you’re in a non-emergency setting, they can refuse to see you if you start visibly marking up their paperwork. And they’ll often insist on the iPad. So be subtle. On both forms, when you get to the signature line, instead of signing your name, write, very legibly: “I do not agree to this.” They’re not checking. They just want the forms back. And later, when they try to hold you to the terms: “Show me where I agreed.”

If any of this is on an iPad instead of paper, just advance the pages to the signature line(s) and write the you-did-not-agree verbiage. Stealthy ninja!

(Are we having fun yet?)

After: When the Bills Start Rolling In

Never pay the first bill.

This is a community creed, borrowed from the late great journalist and health reformer Marshall Allen and his book of the same name — and boy was he spot on.

Explanation of Benefits: The first thing you’ll get is an Explanation of Benefits from your insurance company in the mail or in your online portal. It looks like a bill but it’s not — and it’ll say so in the fine print. It tells you what the doctor or hospital charged, what insurance is paying, and what’s left for you. This is useful information. Hang onto it.

Inadequate Bill: Then the actual hospital or doctor bill arrives with a vague description of service, a date and a number — do not pay it.

Call the number on the bill and say: “I want an itemized bill with CPT codes.”

(Remember those? You’re already an expert here.)

Itemized Bill: This is where it gets interesting. When they have to lay out every line item, the bottom line charge frequently drops compared to the first bill they sent you. Sometimes dramatically. Because they were padding the bill with charges they were hoping you’d never question.

Check the math. Once you have the itemized bill, you can check the math using the procedure we outlined above. Is it “reasonable” as a percentage of Medicare? Does it match their price transparency filings? The Good Faith Estimate? Is it six hundred percent of Medicare?

Pay what’s fair. Now here’s the move — pay what’s fair. I recommend 150 percent of Medicare for a hospital bill and, if you’re feeling generous, 180 percent for a doctor bill — NOT whatever the bill demands when you receive it. But to make sure this works well, you also want to…

Include a “Demand Letter.” Sounds ominous, but it’s actually very simple. Mine goes something like this:

“I didn’t agree to this price in advance. You never disclosed it. It wasn’t in my Good Faith Estimate (or it’s well above the estimate). I can’t find it on your transparency filings (or worse, you didn’t make transparency filings). And check my consent form — I didn’t agree to it.

Under the Uniform Commercial Code, when there is no agreed-upon price in advance, the highest price that can be charged is the price a judge would find reasonable. I assert that 150 percent of Medicare is reasonable. In fact, I’ve already paid you that amount. Please zero out my remaining balance.”

I’ve used this letter. Multiple times. It works.

They won’t write back and say “gosh, you caught us!” They’ll just quietly stop chasing you. The first time I did this, I kept calling like a lunatic. “Have you zeroed out my balance yet?” “Have you zeroed out my balance yet?” “Have you…” Then one day I checked my portal and it was just… zero. No fanfare. No apology. Just silence and a zero balance. (I’ll take it. And you should too.)

Plan B. If that doesn’t work, take that same letter to any lawyer in town. Have them put it on their letterhead and serve it via legal process to the hospital’s registered agent (they’ll know how to do this). Might cost you $200–500, but if it saves you thousands, that’s an ROI you can take to the bank.

One last note on collections.

If collections contacts you while you’re in this process, respond immediately, in writing or on a recorded call.

Say this: “This bill is actively under dispute. I do not accept that I owe this amount.”

They cannot report you to the credit bureaus while you’re actively disputing. So just make it clear that you are disputing. Document it. And do not panic.

The System Is Not Going to Tell You Any Of This.

A lot of these pro-tips exist because of government rules — many of which I personally fought for from inside the White House.

But the system has zero incentive to make any of this easy for you.

Hospitals profit from your confusion. Insurers profit from your passivity. And those iPad forms are designed to strip away the very protections we built for you.

Don’t let them take you to the cleaners.

Walk in knowing the math. Edit the forms. Demand the itemized bill. Pay what’s fair — and not one dollar more.

You are not a child in this system. You’re not a serf. You are the customer. And it’s high time they started treating you like it.

P.S. Before you go, I know I already asked, but this article means everything to me — and it’s free. I gave decades of my life to help create these protections and I desperately want patients to understand how to use them.

After you share, come find me in the comments. I want to hear your billing horror stories. Or your ninja victories. Both are welcome here.

Katy - I’m about to send it to everyone I know. Me and my 350 million homies need the gold that’s in it. Thanks for writing it. Let’s help the people we love save themselves. 🥰

Thanks so much Moorea! I hope it doesn’t come to that for everyone!!